Why New Zealand is an Overlooked AI Hyperscaler Opportunity

'Flops in the wop-wops'

While higher latency and electricity costs make New Zealand a middling candidate for startup-scale datacentres, recent legislative changes help create an exceptionally low-risk environment for AI training. Further, world-class geothermal resources give New Zealand substantial additional generation capacity, which can be scaled to meet demand.

Summary:

2024 regulatory changes have created a ‘fast track’ process where developers can receive certainty in short order. The process does not give carte blanche to ignore environmental issues, but approvals are final and have the same legal force as legislation1.

Approx ~200MW of geothermal capacity is already consented and awaiting investment. ~1GW of technically assessed conventional geothermal is available. Solar and wind capacity is high and growing rapidly, supplementing a stable majority hydroelectric baseload.

Ease of doing business. New Zealand is geopolitically aligned, with modern logistics networks and a highly educated and English-speaking workforce. American citizens can travel visa-free, and work visas are easily obtainable for technical specialists staying in the country for an extended period.

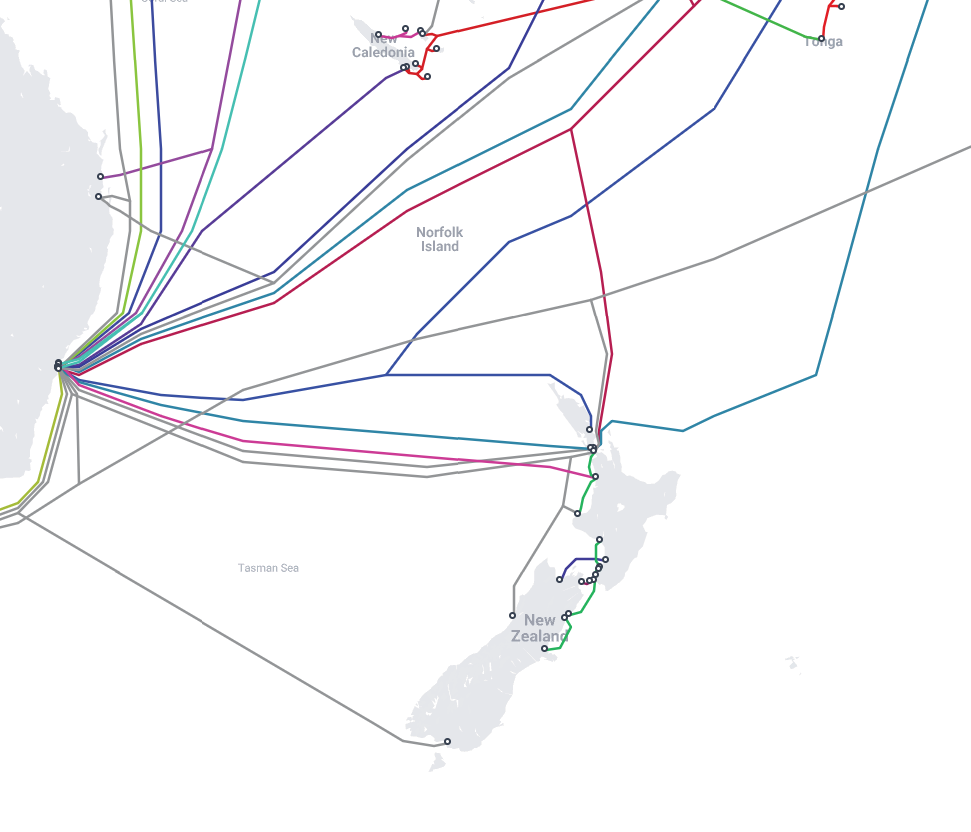

Given its remote location, New Zealand has a latency of ~150ms to US servers, but is connected to North America and Australia by a growing number of high-bandwidth undersea data cables with considerable redundancy.

Regulatory Approvals

The sheer size of modern datacentres, often running to above 100ha for a single campus, are not well suited to Western planning regimes where any minor snag can derail the entire project. Even receiving approval is no guarantee that the project will be able to proceed, as lengthy review processes can extend project timelines indefinitely. By some estimates, over $64b of investment has been blocked or delayed in the US since 2023. Some recent examples:

In September 2024, a $200m Google datacentre planned for Santiago had its permit revoked over water-usage concerns that were already addressed in the lengthy permit process, forcing Google to start from scratch.

In November 2024, Meta AI was forced to abandon a multi-billion-dollar centre in the US after an environmental survey found the presence of a rare bee at the site.

In May 2025, Amazon Web Services (AWS) was forced to suspend a permitted centre after being unable to secure ‘certificates of need’ for 250 backup generators. Frankly, it’s unclear to me what business the state has in determining whether backup generators are necessary for an enormous datacentre.

New Zealand has not been immune to such difficulties. In 2023, after a lengthy process to resolve the issue of needing to drain an artificial pond (‘wetland’), a $7.5b AWS datacentre was held up after the developers were required to demonstrate that stormwater discharges (i.e. from the roof) would not accelerate erosion of the nearby urban creek. Proving such a negative is obviously a considerable challenge, and the project remains indefinitely on hold.

As I’ve discussed previously, modern permitting has become deeply dysfunctional. In attempting to myopically address every minor coordination problem, we create much bigger ones. Resources that could be devoted to securing better outcomes at the system level are instead used to eliminate every minor effect of a project. We’ll spend billions ensuring some discharges are perfectly clean, instead of investing a fraction of that in much better outcomes for the receiving environment as a whole.

Solving this sort of problem is one of the key drivers behind New Zealand’s long-running efforts to reform regulatory planning. The aim of the latest round is to simplify the process, targeting a 45% reduction in costs. These changes are expected to be in place by mid-2026. In the meantime, the Fast-Track Approvals Act 2024 allows projects of ‘regional or national benefit’ (large datacentres have already qualified) to bypass the soon-to-be-repealed process and receive expedited approval directly from the government. Judicial review is permitted, but only within 20 days, and only on points of law, not merit. While projects have been declined on environmental grounds, the new process allows developers to quickly receive certainty about whether a develop can proceed, rather than risk being mired in endless reviews. More information can be found here.

Energy Generation

Another major barrier to datacentre development is the availability of power. After decades of energy efficiency improvements, electricity generation capacity has flatlined since 2007, reflecting an overall per capita decline. The sudden demand for electricity for AI datacentres has left generators flat-footed and struggling to provide capacity, particularly given the permitting dynamics discussed above.

While the price of electricity is relatively high in New Zealand, costing industrial users 0.107USD/kWh in 2024, the country is adding solar and wind generation rapidly, and has hundreds of MWs of geothermal generation capacity already permitted and under construction, or awaiting final investment decision. New Zealand has among the best geothermal resources in the world, currently generating 1055MW, with a further 3GW of assessed conventional capacity yet to be developed2. Government-backed development of deeper ‘supercritical’ geothermal could double this within the next decade, perhaps sooner with demand-driven motivation and investment.

Hyperscalers looking to secure additional generative capacity will be pushing against an open door. The country is now installing solar rapidly, and the government is prioritising speeding the development of both generative and transmission capacity. Generator companies are particularly keen to secure large, long-term contracts with the flexibility of being able to sell power back into the grid when demand is high, as modern datacentres allow.

New Zealand also benefits from a favourable business environment, with an open electricity market, and recent liberalisation of foreign direct investment rules. Meanwhile, new tax rules passed May 2025, allow businesses to claim 20% of the cost of new assets as an expense, helping incentivise development of both power generation and the datacentres themselves.

Stability and Alignment.

Many AI leaders are privately concerned about the risk of locating strategically important assets in dubiously aligned foreign states. By contrast, New Zealand is an English-speaking and highly educated US ally, governed by the rule of law. We watch your movies, and have long-standing sensitive technology transfer treaties with the US. New Zealand is unlikely to be on any AI-chip export restriction list anytime soon.

New Zealand is an export-driven economy dominated by commodity products like dairy and meat products. This means the country is extremely dependent on low barriers to trade, with both major political parties committed to free trade for generations. The risk of a New Zealand development facing elevated tariffs or trade barriers on datacentre components is remote in the extreme - any such act would risk destroying the New Zealand economy.

Skilled Labour

In the current boom, many datacentre developments have been struggling to secure enough skilled labour to avoid delays and cost overruns. Global skill shortages notwithstanding, bringing in outside expertise to New Zealand is relatively easy, and unhindered by annual visa cap systems like the US and EU. ~OECD citizens can enter New Zealand for up to 3 months visa-free. Technical specialists needing to stay for up to 5 years can use a Specific Purpose Work Visa or an Accredited Employer Work Visa. Processing times are 3 - 5 weeks. The system is not entirely without friction - foreign electrical workers will need to be registered locally. The registration process can take up to 8 weeks; however, in the interim, individuals can be issued a limited certificate allowing them to start work immediately under a locally certified supervisor.

Of course, New Zealanders themselves are highly educated and the local labour market is the least restrictive across all English-speaking countries. Unions are active, but employment relations are relatively stable. Days lost due to strike in NZ in 2023 were a third of the UK’s, and less than a tenth of Canada’s. Further, New Zealand is currently experiencing a slowdown in construction activity, leaving spare capacity for early movers. Meanwhile, the geothermal labour side is well covered by a highly mature industry - NZ exports its geothermal expertise globally.

Data Bandwidth

New Zealand’s remote location at the bottom of the Western Pacific makes it generally unsuitable for traditional datacentres. ~150ms of additional ping to US servers is untenable for most gaming or video applications. However, this limitation is essentially irrelevant for AI training, which takes place over weeks or months, or modern chain-of-thought inference, which usually takes seconds to minutes to produce an answer for the user.

Despite the distances involved, New Zealand is well served by a growing set of high-bandwidth undersea cables connecting the islands to Australia and North America. New connections are constantly being added across multiple landing points, making New Zealand’s data connections highly resilient to any single point of failure.

Logistics

Most datacentre components arrive by sea; overland logistics are difficult. Large high-voltage transformers, for example, can exceed 4m in their shortest dimension, making navigation of low bridges and other infrastructure challenging, especially over longer distances. Thus, despite New Zealand’s remoteness, constructing large datacentres here is logistically straightforward. Whether construction takes place in Southland near the new undersea cables and existing hydroelectric capacity there, or in the area surrounding the ‘Taupo Volcanic Zone’ of high geothermal potential - the development will be surrounded by numerous first-rate ports within ~100km, and well-connected by road and rail. Both locations are in predominantly rural areas where land is relatively cheap, yet still close to major cities and service towns alike, so ongoing servicing and maintenance are easy.

Given its remote location and small population3, it's no surprise that the details of New Zealand’s regulatory frameworks or geothermal capacity fail to register in America. Yet, as we’ve seen, the country offers a hyperscaler development location with high capacity and low investment risk where the right people are easily connected in order to make things happen. Please feel free to reach out if you’d like any help with initial introductions.

Following approval, appeals can only be made on points of law, and only within 20 days of the approval being made. Judicial reviews on the merit of the application (e.g. whether the benefits justified the costs) are proscribed by law.

For example, Mercury Energy, in its June 2025 Investor Day presentation, said it was working on a pipeline of ~600MW of geothermal capacity, which could be expedited if demand was evident.

New Zealand’s population is just 5.2 million, spread over a large landmass stretching from the equivalent of New Orleans to Milwaukee.

I think the Invest New Zealand agency should probably read this article...

Wouldn't the same logic -- but with better latency / general connectivity to US / EU markets -- apply to Iceland?